EXHIBIT99

Published on November 18, 2020

November 18, 2020

Contact: HMC Investor Relations Telephone: 205.987.5500

E-mail: irelations@harbert.net

Harbert Discovery Fund Issues Letter to Enzo Biochem Board of Directors

Birmingham, AL, November 18, 2020

Elazar Rabbani, Dov Perlysky, Rebecca Fischer,

We are writing to demand Elazar Rabbani immediately resign as CEO and from the Board of Directors (the “Board”) of Enzo Biochem, Inc. (NYSE: ENZ) (“Enzo” or the “Company”). Harbert Discovery Fund, LP and Harbert Discovery Co-Investment Fund I, LP (collectively “HDF”) currently own approximately 11.74% of the outstanding shares of Enzo, making us the Company’s largest shareholder.

As you will recall, despite your attempts to further entrench the Board during the last proxy campaign, shareholders overwhelmingly voted to elect Fabian Blank and Pete Clemens as directors on February 25, 2020 largely because of their desire to see change at Enzo. Shareholders voted for Pete and Fabian because of the Company’s long history of underperformance, significant share price declines, and disillusionment with a management team that clearly places its own interests ahead of shareholders. It is no surprise that the fundamental results began to improve after Pete and Fabian joined the Board. Based on the timing and unexpected nature of Fabian and Pete’s resignations, it appears that Chairman and CEO Rabbani has created such an extremely hostile environment that Pete and Fabian found their position untenable as minority members in opposition to Mr. Rabbani’s continued mismanagement.

Upon disclosing the resignations of Pete and Fabian, Enzo announced that preliminary revenue for fiscal Q1 exceeded $27 million, the highest revenue quarter the Company has achieved in years. Enzo is clearly benefitting from the increased demand for COVID-19 testing, and we expect this dynamic to continue. It speaks volumes that despite the positive revenue news, shares traded down around 2.5%.

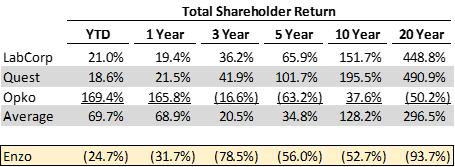

This trading behavior clearly reflects shareholders’ fundamental distrust and frustration with management and the remaining directors. This decline extended the shares year-to-date declines to -25%. Conversely, other public companies benefitting from COVID-19 testing have generated outsized shareholder returns in 2020. Opko, LabCorp, and Quest Diagnostics generated 2020 year-to-date shareholder returns of 169%, 21%, and 19%, respectively. For Enzo, 2020 is a continuation of a long-history of dramatic underperformance.

|

Note: Data per Bloomberg as of November 17, 2020. |

Elazar Rabbani has controlled and mismanaged Enzo for over 40 years. He has consistently paid himself bonuses in spite of negative shareholder returns, he has overseen numerous conflicts of interest, and he has failed to create shareholder value. We have spoken with numerous former employees and not a single one has anything positive to say about his leadership or character. There is a consistent theme that he cares more about maintaining control of the Company than supporting his employees, or creating value for shareholders.

Enough is enough. It is time for the remaining “independent” directors to demand Elazar’s immediate resignation. Upon his resignation, the Company should immediately pursue a sale. M&A multiples are increasing, based on the current demand for lab assets. We believe at a minimum the Company could realize 2x revenues in a sale. Based on recently announced run-rate Q1 fiscal 2021 revenue, that would result in $5.51 per share, or 178% upside from current levels. This is clearly a better option for shareholders than continuing with the current status quo, where even positive fundamental results send the stock down as a result of the extreme and justified distrust of Elazar Rabbani. It is worth noting that the Company has not updated shareholders on the status of its engagement with Lazard since January of 2020. We believe they deserve an update.

Investors are left to ponder what independent directors Perlysky and Fischer stand to benefit from Elazar’s continued entrenchment. Evidently, they have placed their own interest in furthering Elazar’s unscrupulous behavior and self-dealing ways ahead of thousands of individual and institutional investors.

We hope that recently added director Mary Tagliaferri is truly independent and capable of an unbiased assessment of Enzo’s management. Time will tell.

Should directors Perlysky and Fischer refuse to recognize the mandate for change from shareholders and exhibit a preference for systemic cronyism, then at a minimum we request that the Board hire an independent, reputable law firm to investigate Elazar’s various conflicts.

Shareholders deserve better. You can do better. It is a shame and blight on your and Enzo’s reputations that you won’t.

Sincerely,

Harbert Discovery Fund, LP

Harbert Discovery Co-Investment Fund I, LP

Kenan Lucas, Managing Director and Portfolio Manager of Harbert Discovery Fund GP, LLC and Harbert Discovery Co-Investment Fund I GP, LLC

Important Disclosure

THIS STATEMENT CONTAINS OUR CURRENT VIEWS ON THE VALUE OF SECURITIES OF ENZO BIOCHEM, INC. (“ENZO”). OUR VIEWS ARE BASED ON OUR ANALYSIS OF PUBLICLY AVAILABLE INFORMATION AND ASSUMPTIONS WE BELIEVE TO BE REASONABLE. THERE CAN BE NO ASSURANCE THAT THE INFORMATION WE CONSIDERED IS ACCURATE OR COMPLETE, NOR CAN THERE BE ANY ASSURANCE THAT OUR ASSUMPTIONS ARE CORRECT. WE DO NOT RECOMMEND OR ADVISE, NOR DO WE INTEND TO RECOMMEND OR ADVISE, ANY PERSON TO PURCHASE OR SELL SECURITIES AND NO ONE SHOULD RELY ON THIS STATEMENT OR ANY ASPECT OF THIS STATEMENT TO PURCHASE OR SELL SECURITIES OR CONSIDER PURCHASING OR SELLING SECURITIES. THIS STATEMENT DOES NOT PURPORT TO BE, NOR SHOULD IT BE READ, AS AN EXPRESSION OF ANY OPINION OR PREDICTION AS TO THE PRICE AT WHICH ENZO’S SECURITIES MAY TRADE AT ANY TIME. AS NOTED, THIS STATEMENT EXPRESSES OUR CURRENT VIEWS ON ENZO. OUR VIEWS AND OUR HOLDINGS COULD CHANGE AT ANY TIME WITHOUT NOTICE AND WE MAKE NO COMMITMENT TO UPDATE THIS STATEMENT IN THE EVENT OUR VIEWS OR HOLDINGS CHANGE. INVESTORS SHOULD MAKE THEIR OWN DECISIONS REGARDING ENZO AND ITS PROSPECTS WITHOUT RELYING ON, OR EVEN CONSIDERING, ANY OF THE INFORMATION CONTAINED IN THIS STATEMENT.

About Harbert Discovery Fund (“HDF”)

HDF invests in a concentrated portfolio of publicly traded small capitalization companies in the US and Canada. We perform significant due diligence on each portfolio company prior to investing. In addition to researching all publicly available information and meeting with management, our diligence includes substantial primary research with industry experts, consultants, bankers, customers and competitors. We often spend months or years researching ideas before making an investment decision and we only invest in companies that we believe are significantly undervalued, and where there is the potential for change to enhance or accelerate value creation. In an effort to unlock this potential value, we seek to work directly with the boards and management teams of our portfolio companies privately and collaboratively, engaging with them on a range of factors including governance, board composition, corporate strategy, capital allocation, strategic alternatives and operations. We have effected positive, fundamental changes at our current and past investments through this behind-the-scenes, constructive approach. HDF currently has board representation at three of our portfolio companies. In each case, changes to the board were agreed upon privately and it is our strong preference in every investment to avoid the unnecessary distractions and costs of a public proxy campaign.

About Harbert Management Corporation (“HMC”)

HMC is an alternative asset management firm with approximately $7.4 billion in regulatory assets under management as of October 31, 2020. HMC currently sponsors eight distinct investment strategies with dedicated investment teams. Additional information about HMC can be found at www.harbert.net.

###